Tree-Based Methods#

![]()

We import some of our usual libraries at this top level.

import numpy as np

import pandas as pd

from matplotlib.pyplot import subplots

import sklearn.model_selection as skm

from ISLP import load_data, confusion_table

from ISLP.models import ModelSpec as MS

We also collect the new imports needed for this lab.

from sklearn.tree import (DecisionTreeClassifier as DTC,

DecisionTreeRegressor as DTR,

plot_tree,

export_text)

from sklearn.metrics import (accuracy_score,

log_loss)

from sklearn.ensemble import \

(RandomForestRegressor as RF,

GradientBoostingRegressor as GBR)

from ISLP.bart import BART

/Users/jonathantaylor/git-repos/ISLP/ISLP_labs/.venv/lib/python3.12/site-packages/ISLP/bart/likelihood.py:4: SyntaxWarning: invalid escape sequence '\i'

$$ \int_{\mathbb{R}} \frac{1}{(2\pi\sigma^2)^{n/2}} \frac{1}{\sqrt{2

Fitting Classification Trees#

We first use classification trees to analyze the Carseats data set.

In these data, Sales is a continuous variable, and so we begin

by recoding it as a binary variable. We use the where()

function to create a variable, called High, which takes on a

value of Yes if the Sales variable exceeds 8, and takes

on a value of No otherwise.

Carseats = load_data('Carseats')

High = np.where(Carseats.Sales > 8,

"Yes",

"No")

We now use DecisionTreeClassifier() to fit a classification tree in

order to predict High using all variables but Sales.

To do so, we must form a model matrix as we did when fitting regression

models.

model = MS(Carseats.columns.drop('Sales'), intercept=False)

D = model.fit_transform(Carseats)

feature_names = list(D.columns)

X = np.asarray(D)

We have converted D from a data frame to an array X, which is needed in some of the analysis below. We also need the feature_names for annotating our plots later.

There are several options needed to specify the classifier,

such as max_depth (how deep to grow the tree), min_samples_split

(minimum number of observations in a node to be eligible for splitting)

and criterion (whether to use Gini or cross-entropy as the split criterion).

We also set random_state for reproducibility; ties in the split criterion are broken at random.

clf = DTC(criterion='entropy',

max_depth=3,

random_state=0)

clf.fit(X, High)

DecisionTreeClassifier(criterion='entropy', max_depth=3, random_state=0)In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook.

On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

Parameters

In our discussion of qualitative features in Section 3.3,

we noted that for a linear regression model such a feature could be

represented by including a matrix of dummy variables (one-hot-encoding) in the model

matrix, using the formula notation of statsmodels.

As mentioned in Section 8.1, there is a more

natural way to handle qualitative features when building a decision

tree, that does not require such dummy variables; each split amounts to partitioning the levels into two groups.

However,

the sklearn implementation of decision trees does not take

advantage of this approach; instead it simply treats the one-hot-encoded levels as separate variables.

accuracy_score(High, clf.predict(X))

0.79

With only the default arguments, the training error rate is

21%.

For classification trees, we can

access the value of the deviance using log_loss(),

\begin{equation*}

\begin{split}

-2 \sum_m \sum_k n_{mk} \log \hat{p}{mk},

\end{split}

\end{equation*}

where $n{mk}\( is the number of observations in the \)m$th terminal

node that belong to the \(k\)th class.

resid_dev = np.sum(log_loss(High, clf.predict_proba(X)))

resid_dev

np.float64(0.4710647062649358)

This is closely related to the entropy, defined in (8.7). A small deviance indicates a tree that provides a good fit to the (training) data.

One of the most attractive properties of trees is that they can

be graphically displayed. Here we use the plot() function

to display the tree structure.

ax = subplots(figsize=(12,12))[1]

plot_tree(clf,

feature_names=feature_names,

ax=ax);

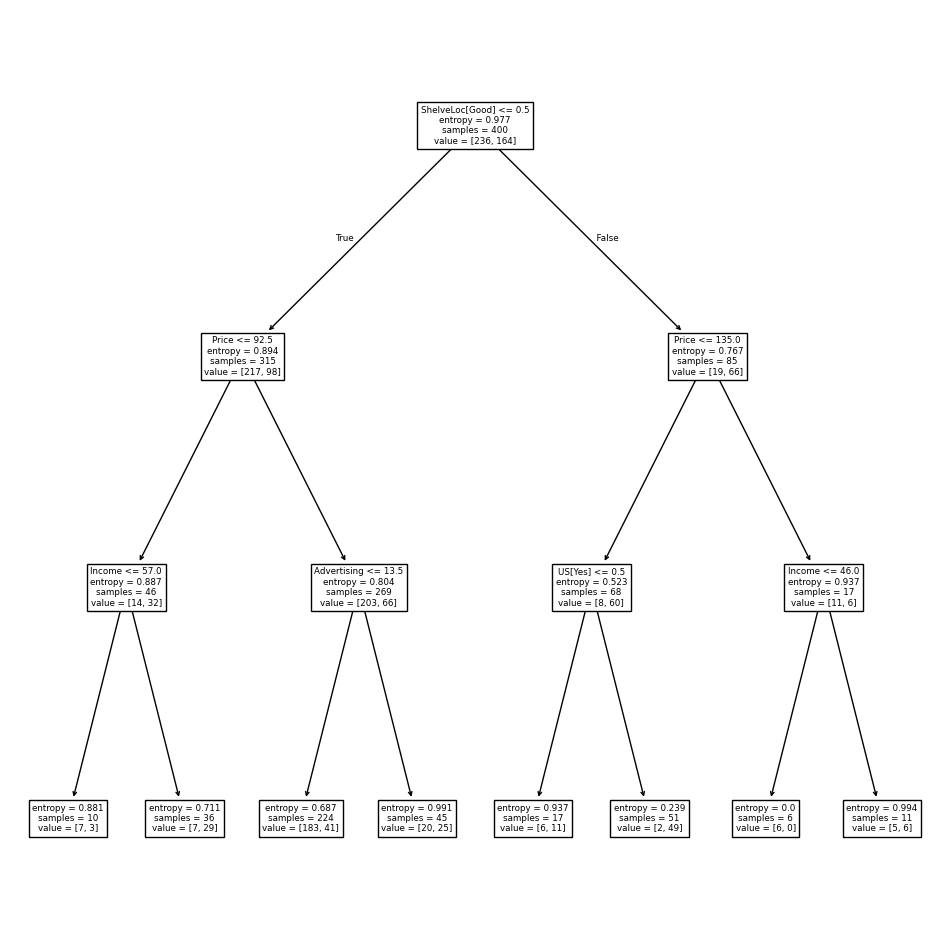

The most important indicator of Sales appears to be ShelveLoc.

We can see a text representation of the tree using

export_text(), which displays the split

criterion (e.g. Price <= 92.5) for each branch.

For leaf nodes it shows the overall prediction

(Yes or No).

We can also see the number of observations in that

leaf that take on values of Yes and No by specifying show_weights=True.

print(export_text(clf,

feature_names=feature_names,

show_weights=True))

|--- ShelveLoc[Good] <= 0.50

| |--- Price <= 92.50

| | |--- Income <= 57.00

| | | |--- weights: [7.00, 3.00] class: No

| | |--- Income > 57.00

| | | |--- weights: [7.00, 29.00] class: Yes

| |--- Price > 92.50

| | |--- Advertising <= 13.50

| | | |--- weights: [183.00, 41.00] class: No

| | |--- Advertising > 13.50

| | | |--- weights: [20.00, 25.00] class: Yes

|--- ShelveLoc[Good] > 0.50

| |--- Price <= 135.00

| | |--- US[Yes] <= 0.50

| | | |--- weights: [6.00, 11.00] class: Yes

| | |--- US[Yes] > 0.50

| | | |--- weights: [2.00, 49.00] class: Yes

| |--- Price > 135.00

| | |--- Income <= 46.00

| | | |--- weights: [6.00, 0.00] class: No

| | |--- Income > 46.00

| | | |--- weights: [5.00, 6.00] class: Yes

In order to properly evaluate the performance of a classification tree on these data, we must estimate the test error rather than simply computing the training error. We split the observations into a training set and a test set, build the tree using the training set, and evaluate its performance on the test data. This pattern is similar to that in Chapter 6, with the linear models replaced here by decision trees — the code for validation is almost identical. This approach leads to correct predictions for 68.5% of the locations in the test data set.

validation = skm.ShuffleSplit(n_splits=1,

test_size=200,

random_state=0)

results = skm.cross_validate(clf,

D,

High,

cv=validation)

results['test_score']

array([0.685])

Next, we consider whether pruning the tree might lead to improved classification performance. We first split the data into a training and test set. We will use cross-validation to prune the tree on the training set, and then evaluate the performance of the pruned tree on the test set.

(X_train,

X_test,

High_train,

High_test) = skm.train_test_split(X,

High,

test_size=0.5,

random_state=0)

We first refit the full tree on the training set; here we do not set a max_depth parameter, since we will learn that through cross-validation.

clf = DTC(criterion='entropy', random_state=0)

clf.fit(X_train, High_train)

accuracy_score(High_test, clf.predict(X_test))

0.735

Next we use the cost_complexity_pruning_path() method of

clf to extract cost-complexity values.

ccp_path = clf.cost_complexity_pruning_path(X_train, High_train)

kfold = skm.KFold(10,

random_state=1,

shuffle=True)

This yields a set of impurities and \(\alpha\) values from which we can extract an optimal one by cross-validation.

grid = skm.GridSearchCV(clf,

{'ccp_alpha': ccp_path.ccp_alphas},

refit=True,

cv=kfold,

scoring='accuracy')

grid.fit(X_train, High_train)

grid.best_score_

np.float64(0.685)

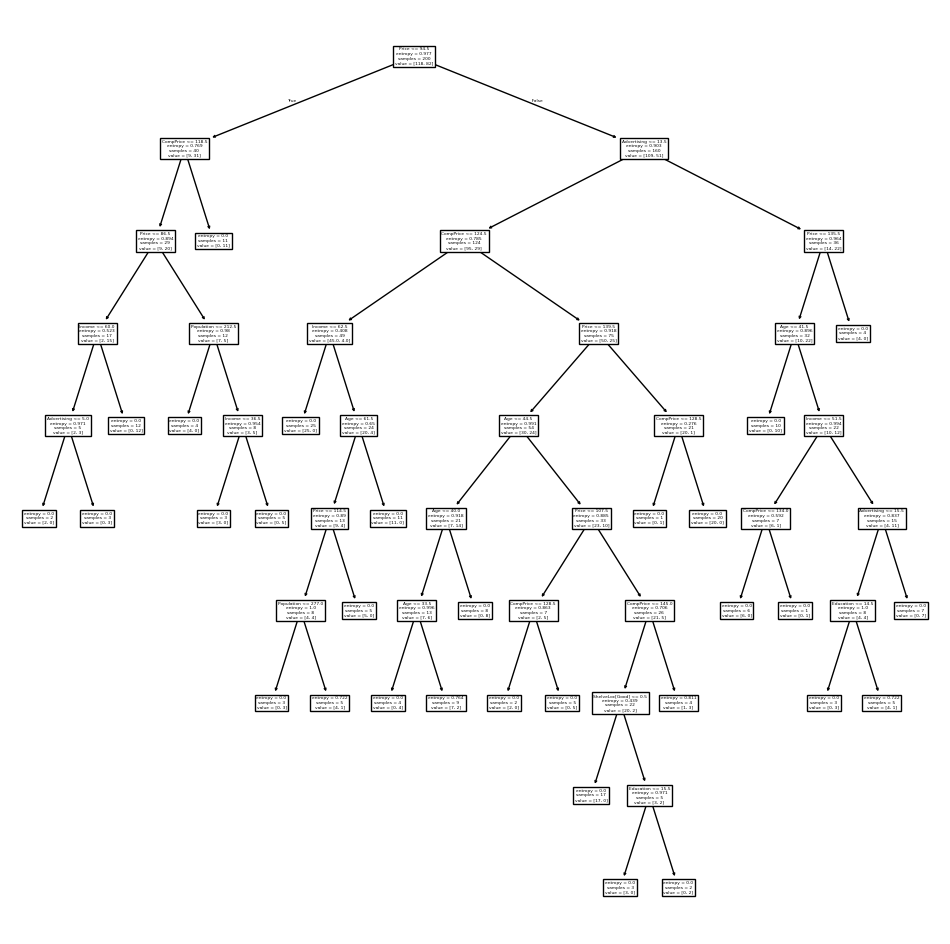

Let’s take a look at the pruned tree.

ax = subplots(figsize=(12, 12))[1]

best_ = grid.best_estimator_

plot_tree(best_,

feature_names=feature_names,

ax=ax);

This is quite a bushy tree. We could count the leaves, or query

best_ instead.

best_.tree_.n_leaves

np.int64(30)

The tree with 30 terminal

nodes results in the lowest cross-validation error rate, with an accuracy of

68.5%. How well does this pruned tree perform on the test data set? Once

again, we apply the predict() function.

print(accuracy_score(High_test,

best_.predict(X_test)))

confusion = confusion_table(best_.predict(X_test),

High_test)

confusion

0.72

| Truth | No | Yes |

|---|---|---|

| Predicted | ||

| No | 94 | 32 |

| Yes | 24 | 50 |

Now 72.0% of the test observations are correctly classified, which is slightly worse than the error for the full tree (with 35 leaves). So cross-validation has not helped us much here; it only pruned off 5 leaves, at a cost of a slightly worse error. These results would change if we were to change the random number seeds above; even though cross-validation gives an unbiased approach to model selection, it does have variance.

Fitting Regression Trees#

Here we fit a regression tree to the Boston data set. The

steps are similar to those for classification trees.

Boston = load_data("Boston")

model = MS(Boston.columns.drop('medv'), intercept=False)

D = model.fit_transform(Boston)

feature_names = list(D.columns)

X = np.asarray(D)

First, we split the data into training and test sets, and fit the tree to the training data. Here we use 30% of the data for the test set.

(X_train,

X_test,

y_train,

y_test) = skm.train_test_split(X,

Boston['medv'],

test_size=0.3,

random_state=0)

Having formed our training and test data sets, we fit the regression tree.

reg = DTR(max_depth=3)

reg.fit(X_train, y_train)

ax = subplots(figsize=(12,12))[1]

plot_tree(reg,

feature_names=feature_names,

ax=ax);

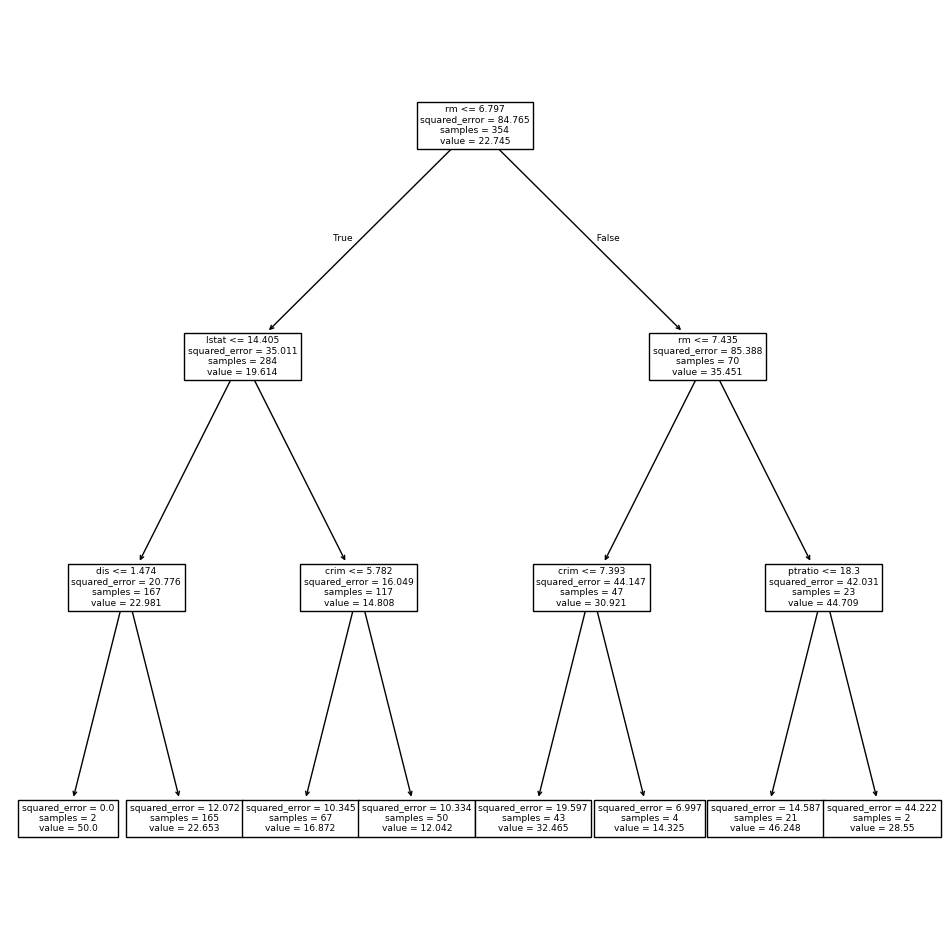

The variable lstat measures the percentage of individuals with

lower socioeconomic status. The tree indicates that lower

values of lstat correspond to more expensive houses.

The tree predicts a median house price of $12,042 for small-sized homes (rm < 6.8), in

suburbs in which residents have low socioeconomic status (lstat > 14.4) and the crime-rate is moderate (crim > 5.8).

Now we use the cross-validation function to see whether pruning the tree will improve performance.

ccp_path = reg.cost_complexity_pruning_path(X_train, y_train)

kfold = skm.KFold(5,

shuffle=True,

random_state=10)

grid = skm.GridSearchCV(reg,

{'ccp_alpha': ccp_path.ccp_alphas},

refit=True,

cv=kfold,

scoring='neg_mean_squared_error')

G = grid.fit(X_train, y_train)

In keeping with the cross-validation results, we use the pruned tree to make predictions on the test set.

best_ = grid.best_estimator_

np.mean((y_test - best_.predict(X_test))**2)

np.float64(28.06985754975404)

In other words, the test set MSE associated with the regression tree is 28.07. The square root of the MSE is therefore around 5.30, indicating that this model leads to test predictions that are within around $5300 of the true median home value for the suburb.

Let’s plot the best tree to see how interpretable it is.

ax = subplots(figsize=(12,12))[1]

plot_tree(G.best_estimator_,

feature_names=feature_names,

ax=ax);

Bagging and Random Forests#

Here we apply bagging and random forests to the Boston data, using

the RandomForestRegressor() from the sklearn.ensemble package. Recall

that bagging is simply a special case of a random forest with

\(m=p\). Therefore, the RandomForestRegressor() function can be used to

perform both bagging and random forests. We start with bagging.

bag_boston = RF(max_features=X_train.shape[1], random_state=0)

bag_boston.fit(X_train, y_train)

RandomForestRegressor(max_features=12, random_state=0)In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook.

On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

Parameters

The argument max_features indicates that all 12 predictors should

be considered for each split of the tree — in other words, that

bagging should be done. How well does this bagged model perform on

the test set?

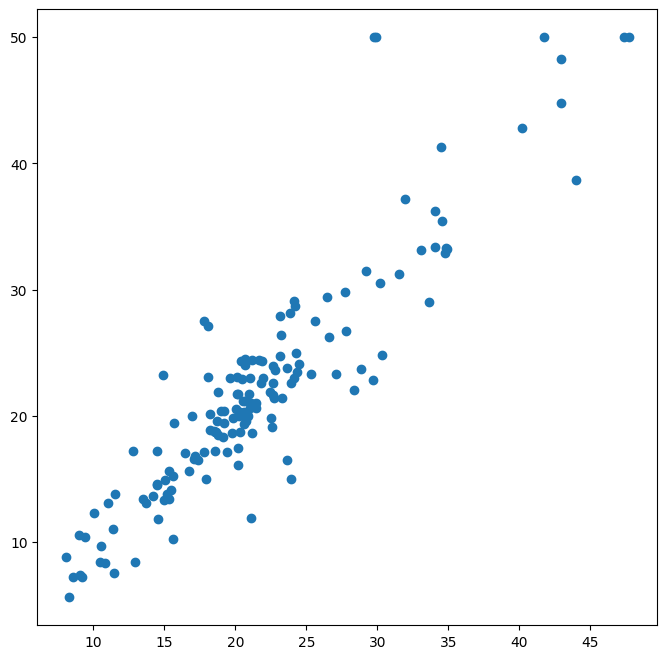

ax = subplots(figsize=(8,8))[1]

y_hat_bag = bag_boston.predict(X_test)

ax.scatter(y_hat_bag, y_test)

np.mean((y_test - y_hat_bag)**2)

np.float64(14.684333796052627)

The test set MSE associated with the bagged regression tree is

14.63, about half that obtained using an optimally-pruned single

tree. We could change the number of trees grown from the default of

100 by

using the n_estimators argument:

bag_boston = RF(max_features=X_train.shape[1],

n_estimators=500,

random_state=0).fit(X_train, y_train)

y_hat_bag = bag_boston.predict(X_test)

np.mean((y_test - y_hat_bag)**2)

np.float64(14.565312103157904)

There is not much change. Bagging and random forests cannot overfit by increasing the number of trees, but can underfit if the number is too small.

Growing a random forest proceeds in exactly the same way, except that

we use a smaller value of the max_features argument. By default,

RandomForestRegressor() uses \(p\) variables when building a random

forest of regression trees (i.e. it defaults to bagging), and RandomForestClassifier() uses

\(\sqrt{p}\) variables when building a

random forest of classification trees. Here we use max_features=6.

RF_boston = RF(max_features=6,

random_state=0).fit(X_train, y_train)

y_hat_RF = RF_boston.predict(X_test)

np.mean((y_test - y_hat_RF)**2)

np.float64(19.998839111842113)

The test set MSE is 20.04;

this indicates that random forests did somewhat worse than bagging

in this case. Extracting the feature_importances_ values from the fitted model, we can view the

importance of each variable.

feature_imp = pd.DataFrame(

{'importance':RF_boston.feature_importances_},

index=feature_names)

feature_imp.sort_values(by='importance', ascending=False)

| importance | |

|---|---|

| lstat | 0.353808 |

| rm | 0.334349 |

| ptratio | 0.069519 |

| crim | 0.056386 |

| indus | 0.053183 |

| dis | 0.043762 |

| nox | 0.033085 |

| tax | 0.025047 |

| age | 0.019238 |

| rad | 0.005169 |

| chas | 0.004331 |

| zn | 0.002123 |

This

is a relative measure of the total decrease in node impurity that results from

splits over that variable, averaged over all trees (this was plotted in Figure 8.9 for a model fit to the Heart data).

The results indicate that across all of the trees considered in the

random forest, the wealth level of the community (lstat) and the

house size (rm) are by far the two most important variables.

Boosting#

Here we use GradientBoostingRegressor() from sklearn.ensemble

to fit boosted regression trees to the Boston data

set. For classification we would use GradientBoostingClassifier().

The argument n_estimators=5000

indicates that we want 5000 trees, and the option

max_depth=3 limits the depth of each tree. The

argument learning_rate is the \(\lambda\)

mentioned earlier in the description of boosting.

boost_boston = GBR(n_estimators=5000,

learning_rate=0.001,

max_depth=3,

random_state=0)

boost_boston.fit(X_train, y_train)

GradientBoostingRegressor(learning_rate=0.001, n_estimators=5000,

random_state=0)In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook. On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

Parameters

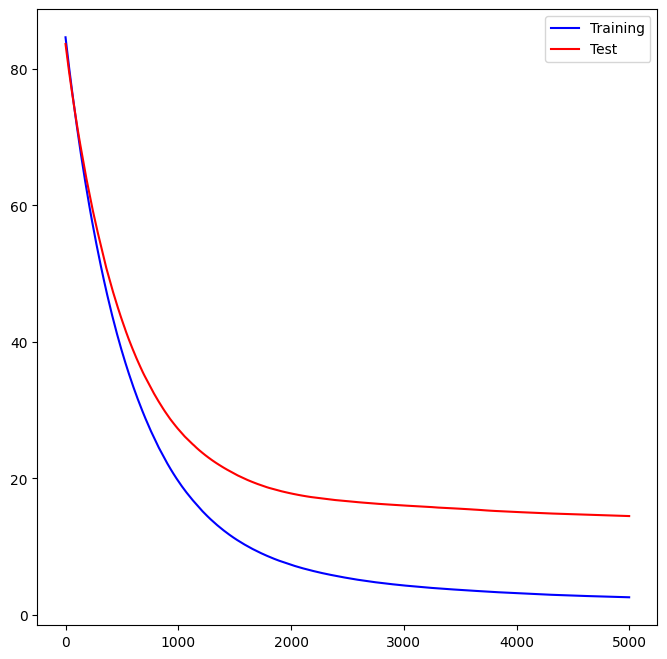

We can see how the training error decreases with the train_score_ attribute.

To get an idea of how the test error decreases we can use the

staged_predict() method to get the predicted values along the path.

test_error = np.zeros_like(boost_boston.train_score_)

for idx, y_ in enumerate(boost_boston.staged_predict(X_test)):

test_error[idx] = np.mean((y_test - y_)**2)

plot_idx = np.arange(boost_boston.train_score_.shape[0])

ax = subplots(figsize=(8,8))[1]

ax.plot(plot_idx,

boost_boston.train_score_,

'b',

label='Training')

ax.plot(plot_idx,

test_error,

'r',

label='Test')

ax.legend();

We now use the boosted model to predict medv on the test set:

y_hat_boost = boost_boston.predict(X_test);

np.mean((y_test - y_hat_boost)**2)

np.float64(14.478980532887332)

The test MSE obtained is 14.48, similar to the test MSE for bagging. If we want to, we can perform boosting with a different value of the shrinkage parameter \(\lambda\) in (8.10). The default value is 0.001, but this is easily modified. Here we take \(\lambda=0.2\).

boost_boston = GBR(n_estimators=5000,

learning_rate=0.2,

max_depth=3,

random_state=0)

boost_boston.fit(X_train,

y_train)

y_hat_boost = boost_boston.predict(X_test);

np.mean((y_test - y_hat_boost)**2)

np.float64(14.501514553719568)

In this case, using \(\lambda=0.2\) leads to almost the same test MSE as when using \(\lambda=0.001\).

Bayesian Additive Regression Trees#

In this section we demonstrate a Python implementation of BART found in the

ISLP.bart package. We fit a model

to the Boston housing data set. This BART() estimator is

designed for quantitative outcome variables, though other implementations are available for

fitting logistic and probit models to categorical outcomes.

bart_boston = BART(random_state=0, burnin=5, ndraw=15)

bart_boston.fit(X_train, y_train)

BART(burnin=5, ndraw=15, random_state=0)In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook.

On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

Parameters

| num_trees | 200 | |

| num_particles | 10 | |

| max_stages | 5000 | |

| split_prob | <function BAR...t 0x110e51580> | |

| min_depth | 0 | |

| std_scale | 2 | |

| split_prior | None | |

| ndraw | 15 | |

| burnin | 5 | |

| sigma_prior | (5, ...) | |

| num_quantile | 50 | |

| random_state | 0 | |

| n_jobs | -1 |

On this data set, with this split into test and training, we see that the test error of BART is similar to that of random forest.

yhat_test = bart_boston.predict(X_test.astype(np.float32))

np.mean((y_test - yhat_test)**2)

np.float64(22.145009458109207)

We can check how many times each variable appeared in the collection of trees. This gives a summary similar to the variable importance plot for boosting and random forests.

var_inclusion = pd.Series(bart_boston.variable_inclusion_.mean(0),

index=D.columns)

var_inclusion

crim 26.933333

zn 27.866667

indus 26.466667

chas 22.466667

nox 26.600000

rm 29.800000

age 22.733333

dis 26.466667

rad 23.666667

tax 24.133333

ptratio 24.266667

lstat 31.000000

dtype: float64