Logistic Regression, LDA, QDA, and KNN#

![]()

The Stock Market Data#

In this lab we will examine the Smarket

data, which is part of the ISLP

library. This data set consists of percentage returns for the S&P 500

stock index over 1,250 days, from the beginning of 2001 until the end

of 2005. For each date, we have recorded the percentage returns for

each of the five previous trading days, Lag1 through

Lag5. We have also recorded Volume (the number of

shares traded on the previous day, in billions), Today (the

percentage return on the date in question) and Direction

(whether the market was Up or Down on this date).

We start by importing our libraries at this top level; these are all imports we have seen in previous labs.

import numpy as np

import pandas as pd

from matplotlib.pyplot import subplots

import statsmodels.api as sm

from ISLP import load_data

from ISLP.models import (ModelSpec as MS,

summarize)

We also collect together the new imports needed for this lab.

from ISLP import confusion_table

from ISLP.models import contrast

from sklearn.discriminant_analysis import \

(LinearDiscriminantAnalysis as LDA,

QuadraticDiscriminantAnalysis as QDA)

from sklearn.naive_bayes import GaussianNB

from sklearn.neighbors import KNeighborsClassifier

from sklearn.preprocessing import StandardScaler

from sklearn.model_selection import train_test_split

from sklearn.linear_model import LogisticRegression

Now we are ready to load the Smarket data.

Smarket = load_data('Smarket')

Smarket

| Year | Lag1 | Lag2 | Lag3 | Lag4 | Lag5 | Volume | Today | Direction | |

|---|---|---|---|---|---|---|---|---|---|

| 0 | 2001 | 0.381 | -0.192 | -2.624 | -1.055 | 5.010 | 1.19130 | 0.959 | Up |

| 1 | 2001 | 0.959 | 0.381 | -0.192 | -2.624 | -1.055 | 1.29650 | 1.032 | Up |

| 2 | 2001 | 1.032 | 0.959 | 0.381 | -0.192 | -2.624 | 1.41120 | -0.623 | Down |

| 3 | 2001 | -0.623 | 1.032 | 0.959 | 0.381 | -0.192 | 1.27600 | 0.614 | Up |

| 4 | 2001 | 0.614 | -0.623 | 1.032 | 0.959 | 0.381 | 1.20570 | 0.213 | Up |

| ... | ... | ... | ... | ... | ... | ... | ... | ... | ... |

| 1245 | 2005 | 0.422 | 0.252 | -0.024 | -0.584 | -0.285 | 1.88850 | 0.043 | Up |

| 1246 | 2005 | 0.043 | 0.422 | 0.252 | -0.024 | -0.584 | 1.28581 | -0.955 | Down |

| 1247 | 2005 | -0.955 | 0.043 | 0.422 | 0.252 | -0.024 | 1.54047 | 0.130 | Up |

| 1248 | 2005 | 0.130 | -0.955 | 0.043 | 0.422 | 0.252 | 1.42236 | -0.298 | Down |

| 1249 | 2005 | -0.298 | 0.130 | -0.955 | 0.043 | 0.422 | 1.38254 | -0.489 | Down |

1250 rows × 9 columns

This gives a truncated listing of the data. We can see what the variable names are.

Smarket.columns

Index(['Year', 'Lag1', 'Lag2', 'Lag3', 'Lag4', 'Lag5', 'Volume', 'Today',

'Direction'],

dtype='str')

We compute the correlation matrix using the corr() method

for data frames, which produces a matrix that contains all of

the pairwise correlations among the variables.

By instructing pandas to use only numeric variables, the corr() method does not report a correlation for the Direction variable because it is

qualitative.

Smarket.corr(numeric_only=True)

| Year | Lag1 | Lag2 | Lag3 | Lag4 | Lag5 | Volume | Today | |

|---|---|---|---|---|---|---|---|---|

| Year | 1.000000 | 0.029700 | 0.030596 | 0.033195 | 0.035689 | 0.029788 | 0.539006 | 0.030095 |

| Lag1 | 0.029700 | 1.000000 | -0.026294 | -0.010803 | -0.002986 | -0.005675 | 0.040910 | -0.026155 |

| Lag2 | 0.030596 | -0.026294 | 1.000000 | -0.025897 | -0.010854 | -0.003558 | -0.043383 | -0.010250 |

| Lag3 | 0.033195 | -0.010803 | -0.025897 | 1.000000 | -0.024051 | -0.018808 | -0.041824 | -0.002448 |

| Lag4 | 0.035689 | -0.002986 | -0.010854 | -0.024051 | 1.000000 | -0.027084 | -0.048414 | -0.006900 |

| Lag5 | 0.029788 | -0.005675 | -0.003558 | -0.018808 | -0.027084 | 1.000000 | -0.022002 | -0.034860 |

| Volume | 0.539006 | 0.040910 | -0.043383 | -0.041824 | -0.048414 | -0.022002 | 1.000000 | 0.014592 |

| Today | 0.030095 | -0.026155 | -0.010250 | -0.002448 | -0.006900 | -0.034860 | 0.014592 | 1.000000 |

As one would expect, the correlations between the lagged return variables and

today’s return are close to zero. The only substantial correlation is between Year and

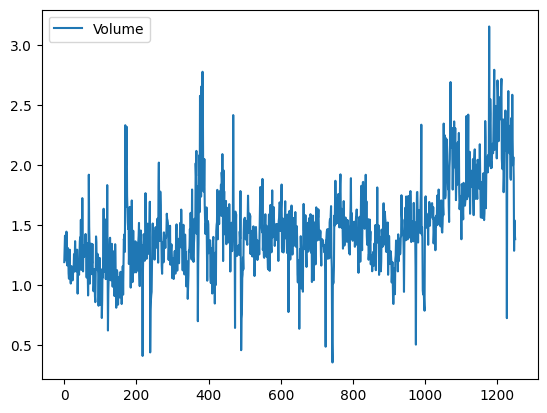

Volume. By plotting the data we see that Volume

is increasing over time. In other words, the average number of shares traded

daily increased from 2001 to 2005.

Smarket.plot(y='Volume');

Logistic Regression#

Next, we will fit a logistic regression model in order to predict

Direction using Lag1 through Lag5 and

Volume. The sm.GLM() function fits generalized linear models, a class of

models that includes logistic regression. Alternatively,

the function sm.Logit() fits a logistic regression

model directly. The syntax of

sm.GLM() is similar to that of sm.OLS(), except

that we must pass in the argument family=sm.families.Binomial()

in order to tell statsmodels to run a logistic regression rather than some other

type of generalized linear model.

allvars = Smarket.columns.drop(['Today', 'Direction', 'Year'])

design = MS(allvars)

X = design.fit_transform(Smarket)

y = Smarket.Direction == 'Up'

glm = sm.GLM(y,

X,

family=sm.families.Binomial())

results = glm.fit()

summarize(results)

| coef | std err | z | P>|z| | |

|---|---|---|---|---|

| intercept | -0.1260 | 0.241 | -0.523 | 0.601 |

| Lag1 | -0.0731 | 0.050 | -1.457 | 0.145 |

| Lag2 | -0.0423 | 0.050 | -0.845 | 0.398 |

| Lag3 | 0.0111 | 0.050 | 0.222 | 0.824 |

| Lag4 | 0.0094 | 0.050 | 0.187 | 0.851 |

| Lag5 | 0.0103 | 0.050 | 0.208 | 0.835 |

| Volume | 0.1354 | 0.158 | 0.855 | 0.392 |

The smallest p-value here is associated with Lag1. The

negative coefficient for this predictor suggests that if the market

had a positive return yesterday, then it is less likely to go up

today. However, at a value of 0.15, the p-value is still

relatively large, and so there is no clear evidence of a real

association between Lag1 and Direction.

We use the params attribute of results

in order to access just the

coefficients for this fitted model.

results.params

intercept -0.126000

Lag1 -0.073074

Lag2 -0.042301

Lag3 0.011085

Lag4 0.009359

Lag5 0.010313

Volume 0.135441

dtype: float64

Likewise we can use the

pvalues attribute to access the p-values for the coefficients.

results.pvalues

intercept 0.600700

Lag1 0.145232

Lag2 0.398352

Lag3 0.824334

Lag4 0.851445

Lag5 0.834998

Volume 0.392404

dtype: float64

The predict() method of results can be used to predict the

probability that the market will go up, given values of the

predictors. This method returns predictions

on the probability scale. If no data set is supplied to the predict()

function, then the probabilities are computed for the training data

that was used to fit the logistic regression model.

As with linear regression, one can pass an optional exog argument consistent

with a design matrix if desired. Here we have

printed only the first ten probabilities.

probs = results.predict()

probs[:10]

array([0.50708413, 0.48146788, 0.48113883, 0.51522236, 0.51078116,

0.50695646, 0.49265087, 0.50922916, 0.51761353, 0.48883778])

In order to make a prediction as to whether the market will go up or

down on a particular day, we must convert these predicted

probabilities into class labels, Up or Down. The

following two commands create a vector of class predictions based on

whether the predicted probability of a market increase is greater than

or less than 0.5.

labels = np.array(['Down']*1250)

labels[probs>0.5] = "Up"

The confusion_table()

function from the ISLP package summarizes these predictions, showing how

many observations were correctly or incorrectly classified. Our function, which is adapted from a similar function

in the module sklearn.metrics, transposes the resulting

matrix and includes row and column labels.

The confusion_table() function takes as first argument the

predicted labels, and second argument the true labels.

confusion_table(labels, Smarket.Direction)

| Truth | Down | Up |

|---|---|---|

| Predicted | ||

| Down | 145 | 141 |

| Up | 457 | 507 |

The diagonal elements of the confusion matrix indicate correct

predictions, while the off-diagonals represent incorrect

predictions. Hence our model correctly predicted that the market would

go up on 507 days and that it would go down on 145 days, for a

total of 507 + 145 = 652 correct predictions. The np.mean()

function can be used to compute the fraction of days for which the

prediction was correct. In this case, logistic regression correctly

predicted the movement of the market 52.2% of the time.

(507+145)/1250, np.mean(labels == Smarket.Direction)

(0.5216, np.float64(0.5216))

At first glance, it appears that the logistic regression model is working a little better than random guessing. However, this result is misleading because we trained and tested the model on the same set of 1,250 observations. In other words, \(100-52.2=47.8%\) is the training error rate. As we have seen previously, the training error rate is often overly optimistic — it tends to underestimate the test error rate. In order to better assess the accuracy of the logistic regression model in this setting, we can fit the model using part of the data, and then examine how well it predicts the held out data. This will yield a more realistic error rate, in the sense that in practice we will be interested in our model’s performance not on the data that we used to fit the model, but rather on days in the future for which the market’s movements are unknown.

To implement this strategy, we first create a Boolean vector corresponding to the observations from 2001 through 2004. We then use this vector to create a held out data set of observations from 2005.

train = (Smarket.Year < 2005)

Smarket_train = Smarket.loc[train]

Smarket_test = Smarket.loc[~train]

Smarket_test.shape

(252, 9)

The object train is a vector of 1,250 elements, corresponding

to the observations in our data set. The elements of the vector that

correspond to observations that occurred before 2005 are set to

True, whereas those that correspond to observations in 2005 are

set to False. Hence train is a

boolean array, since its

elements are True and False. Boolean arrays can be used

to obtain a subset of the rows or columns of a data frame

using the loc method. For instance,

the command Smarket.loc[train] would pick out a submatrix of the

stock market data set, corresponding only to the dates before 2005,

since those are the ones for which the elements of train are

True. The ~ symbol can be used to negate all of the

elements of a Boolean vector. That is, ~train is a vector

similar to train, except that the elements that are True

in train get swapped to False in ~train, and vice versa.

Therefore, Smarket.loc[~train] yields a

subset of the rows of the data frame

of the stock market data containing only the observations for which

train is False.

The output above indicates that there are 252 such

observations.

We now fit a logistic regression model using only the subset of the observations that correspond to dates before 2005. We then obtain predicted probabilities of the stock market going up for each of the days in our test set — that is, for the days in 2005.

X_train, X_test = X.loc[train], X.loc[~train]

y_train, y_test = y.loc[train], y.loc[~train]

glm_train = sm.GLM(y_train,

X_train,

family=sm.families.Binomial())

results = glm_train.fit()

probs = results.predict(exog=X_test)

Notice that we have trained and tested our model on two completely separate data sets: training was performed using only the dates before 2005, and testing was performed using only the dates in 2005.

Finally, we compare the predictions for 2005 to the

actual movements of the market over that time period.

We will first store the test and training labels (recall y_test is binary).

D = Smarket.Direction

L_train, L_test = D.loc[train], D.loc[~train]

Now we threshold the fitted probability at 50% to form our predicted labels.

labels = np.array(['Down']*252)

labels[probs>0.5] = 'Up'

confusion_table(labels, L_test)

| Truth | Down | Up |

|---|---|---|

| Predicted | ||

| Down | 77 | 97 |

| Up | 34 | 44 |

The test accuracy is about 48% while the error rate is about 52%

np.mean(labels == L_test), np.mean(labels != L_test)

(np.float64(0.4801587301587302), np.float64(0.5198412698412699))

The != notation means not equal to, and so the last command

computes the test set error rate. The results are rather

disappointing: the test error rate is 52%, which is worse than

random guessing! Of course this result is not all that surprising,

given that one would not generally expect to be able to use previous

days’ returns to predict future market performance. (After all, if it

were possible to do so, then the authors of this book would be out

striking it rich rather than writing a statistics textbook.)

We recall that the logistic regression model had very underwhelming

p-values associated with all of the predictors, and that the

smallest p-value, though not very small, corresponded to

Lag1. Perhaps by removing the variables that appear not to be

helpful in predicting Direction, we can obtain a more

effective model. After all, using predictors that have no relationship

with the response tends to cause a deterioration in the test error

rate (since such predictors cause an increase in variance without a

corresponding decrease in bias), and so removing such predictors may

in turn yield an improvement. Below we refit the logistic

regression using just Lag1 and Lag2, which seemed to

have the highest predictive power in the original logistic regression

model.

model = MS(['Lag1', 'Lag2']).fit(Smarket)

X = model.transform(Smarket)

X_train, X_test = X.loc[train], X.loc[~train]

glm_train = sm.GLM(y_train,

X_train,

family=sm.families.Binomial())

results = glm_train.fit()

probs = results.predict(exog=X_test)

labels = np.array(['Down']*252)

labels[probs>0.5] = 'Up'

confusion_table(labels, L_test)

| Truth | Down | Up |

|---|---|---|

| Predicted | ||

| Down | 35 | 35 |

| Up | 76 | 106 |

Let’s evaluate the overall accuracy as well as the accuracy within the days when logistic regression predicts an increase.

(35+106)/252,106/(106+76)

(0.5595238095238095, 0.5824175824175825)

Now the results appear to be a little better: 56% of the daily movements have been correctly predicted. It is worth noting that in this case, a much simpler strategy of predicting that the market will increase every day will also be correct 56% of the time! Hence, in terms of overall error rate, the logistic regression method is no better than the naive approach. However, the confusion matrix shows that on days when logistic regression predicts an increase in the market, it has a 58% accuracy rate. This suggests a possible trading strategy of buying on days when the model predicts an increasing market, and avoiding trades on days when a decrease is predicted. Of course one would need to investigate more carefully whether this small improvement was real or just due to random chance.

Suppose that we want to predict the returns associated with particular

values of Lag1 and Lag2. In particular, we want to

predict Direction on a day when Lag1 and

Lag2 equal \(1.2\) and \(1.1\), respectively, and on a day when they

equal \(1.5\) and \(-0.8\). We do this using the predict()

function.

newdata = pd.DataFrame({'Lag1':[1.2, 1.5],

'Lag2':[1.1, -0.8]});

newX = model.transform(newdata)

results.predict(newX)

0 0.479146

1 0.496094

dtype: float64

Linear Discriminant Analysis#

We begin by performing LDA on the Smarket data, using the function

LinearDiscriminantAnalysis(), which we have abbreviated LDA(). We

fit the model using only the observations before 2005.

lda = LDA(store_covariance=True)

Since the LDA estimator automatically

adds an intercept, we should remove the column corresponding to the

intercept in both X_train and X_test. We can also directly

use the labels rather than the Boolean vectors y_train.

X_train, X_test = [M.drop(columns=['intercept'])

for M in [X_train, X_test]]

lda.fit(X_train, L_train)

LinearDiscriminantAnalysis(store_covariance=True)In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook.

On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

Parameters

Here we have used the list comprehensions introduced

in Section 3.6.4. Looking at our first line above, we see that the right-hand side is a list

of length two. This is because the code for M in [X_train, X_test] iterates over a list

of length two. While here we loop over a list,

the list comprehension method works when looping over any iterable object.

We then apply the drop() method to each element in the iteration, collecting

the result in a list. The left-hand side tells Python to unpack this list

of length two, assigning its elements to the variables X_train and X_test. Of course,

this overwrites the previous values of X_train and X_test.

Having fit the model, we can extract the means in the two classes with the means_ attribute. These are the average of each predictor within each class, and

are used by LDA as estimates of \(\mu_k\). These suggest that there is

a tendency for the previous 2 days’ returns to be negative on days

when the market increases, and a tendency for the previous days’

returns to be positive on days when the market declines.

lda.means_

array([[ 0.04279022, 0.03389409],

[-0.03954635, -0.03132544]])

The estimated prior probabilities are stored in the priors_ attribute.

The package sklearn typically uses this trailing _ to denote

a quantity estimated when using the fit() method. We can be sure of which

entry corresponds to which label by looking at the classes_ attribute.

lda.classes_

array(['Down', 'Up'], dtype='<U4')

The LDA output indicates that \(\hat\pi_{Down}=0.492\) and \(\hat\pi_{Up}=0.508\).

lda.priors_

array([0.49198397, 0.50801603])

The linear discriminant vectors can be found in the scalings_ attribute:

lda.scalings_

array([[-0.64201904],

[-0.51352928]])

These values provide the linear combination of Lag1 and Lag2 that are used to form the LDA decision rule. In other words, these are the multipliers of the elements of \(X=x\) in (4.24).

If $-0.64\times Lag1 - 0.51 \times Lag2 $ is large, then the LDA classifier will predict a market increase, and if it is small, then the LDA classifier will predict a market decline.

lda_pred = lda.predict(X_test)

As we observed in our comparison of classification methods (Section 4.5), the LDA and logistic regression predictions are almost identical.

confusion_table(lda_pred, L_test)

| Truth | Down | Up |

|---|---|---|

| Predicted | ||

| Down | 35 | 35 |

| Up | 76 | 106 |

We can also estimate the

probability of each class for

each point in a training set. Applying a 50% threshold to the posterior probabilities of

being in class one allows us to

recreate the predictions contained in lda_pred.

lda_prob = lda.predict_proba(X_test)

np.all(

np.where(lda_prob[:,1] >= 0.5, 'Up','Down') == lda_pred

)

np.True_

Above, we used the np.where() function that

creates an array with value 'Up' for indices where

the second column of lda_prob (the estimated

posterior probability of 'Up') is greater than 0.5.

For problems with more than two classes the labels are chosen as the class whose posterior probability is highest:

np.all(

[lda.classes_[i] for i in np.argmax(lda_prob, 1)] == lda_pred

)

np.True_

If we wanted to use a posterior probability threshold other than

50% in order to make predictions, then we could easily do so. For

instance, suppose that we wish to predict a market decrease only if we

are very certain that the market will indeed decrease on that

day — say, if the posterior probability is at least 90%.

We know that the first column of lda_prob corresponds to the

label Down after having checked the classes_ attribute, hence we use

the column index 0 rather than 1 as we did above.

np.sum(lda_prob[:,0] > 0.9)

np.int64(0)

No days in 2005 meet that threshold! In fact, the greatest posterior probability of decrease in all of 2005 was 52.02%.

The LDA classifier above is the first classifier from the

sklearn library. We will use several other objects

from this library. The objects

follow a common structure that simplifies tasks such as cross-validation,

which we will see in Chapter 5. Specifically,

the methods first create a generic classifier without

referring to any data. This classifier is then fit

to data with the fit() method and predictions are

always produced with the predict() method. This pattern

of first instantiating the classifier, followed by fitting it, and

then producing predictions is an explicit design choice of sklearn. This uniformity

makes it possible to cleanly copy the classifier so that it can be fit

on different data; e.g. different training sets arising in cross-validation.

This standard pattern also allows for a predictable formation of workflows.

Quadratic Discriminant Analysis#

We will now fit a QDA model to the Smarket data. QDA is

implemented via

QuadraticDiscriminantAnalysis()

in the sklearn package, which we abbreviate to QDA().

The syntax is very similar to LDA().

qda = QDA(store_covariance=True)

qda.fit(X_train, L_train)

QuadraticDiscriminantAnalysis(store_covariance=True)In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook.

On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

Parameters

The QDA() function will again compute means_ and priors_.

qda.means_, qda.priors_

(array([[ 0.04279022, 0.03389409],

[-0.03954635, -0.03132544]]),

array([0.49198397, 0.50801603]))

The QDA() classifier will estimate one covariance per class. Here is the

estimated covariance in the first class:

qda.covariance_[0]

array([[ 1.50662277, -0.03924806],

[-0.03924806, 1.53559498]])

The output contains the group means. But it does not contain the

coefficients of the linear discriminants, because the QDA classifier

involves a quadratic, rather than a linear, function of the

predictors. The predict() function works in exactly the

same fashion as for LDA.

qda_pred = qda.predict(X_test)

confusion_table(qda_pred, L_test)

| Truth | Down | Up |

|---|---|---|

| Predicted | ||

| Down | 30 | 20 |

| Up | 81 | 121 |

Interestingly, the QDA predictions are accurate almost 60% of the time, even though the 2005 data was not used to fit the model.

np.mean(qda_pred == L_test)

np.float64(0.5992063492063492)

This level of accuracy is quite impressive for stock market data, which is known to be quite hard to model accurately. This suggests that the quadratic form assumed by QDA may capture the true relationship more accurately than the linear forms assumed by LDA and logistic regression. However, we recommend evaluating this method’s performance on a larger test set before betting that this approach will consistently beat the market!

Naive Bayes#

Next, we fit a naive Bayes model to the Smarket data. The syntax is

similar to that of LDA() and QDA(). By

default, this implementation GaussianNB() of the naive Bayes classifier models each

quantitative feature using a Gaussian distribution. However, a kernel

density method can also be used to estimate the distributions.

NB = GaussianNB()

NB.fit(X_train, L_train)

GaussianNB()In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook.

On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

Parameters

The classes are stored as classes_.

NB.classes_

array(['Down', 'Up'], dtype='<U4')

The class prior probabilities are stored in the class_prior_ attribute.

NB.class_prior_

array([0.49198397, 0.50801603])

The parameters of the features can be found in the theta_ and var_ attributes. The number of rows

is equal to the number of classes, while the number of columns is equal to the number of features.

We see below that the mean for feature Lag1 in the Down class is 0.043.

NB.theta_

array([[ 0.04279022, 0.03389409],

[-0.03954635, -0.03132544]])

Its variance is 1.503.

NB.var_

array([[1.50355429, 1.53246749],

[1.51401364, 1.48732877]])

How do we know the names of these attributes? We use NB? (or ?NB).

We can easily verify the mean computation:

X_train[L_train == 'Down'].mean()

Lag1 0.042790

Lag2 0.033894

dtype: float64

Similarly for the variance:

X_train[L_train == 'Down'].var(ddof=0)

Lag1 1.503554

Lag2 1.532467

dtype: float64

Since NB() is a classifier in the sklearn library, making predictions

uses the same syntax as for LDA() and QDA() above.

nb_labels = NB.predict(X_test)

confusion_table(nb_labels, L_test)

| Truth | Down | Up |

|---|---|---|

| Predicted | ||

| Down | 29 | 20 |

| Up | 82 | 121 |

Naive Bayes performs well on these data, with accurate predictions over 59% of the time. This is slightly worse than QDA, but much better than LDA.

As for LDA, the predict_proba() method estimates the probability that each observation belongs to a particular class.

NB.predict_proba(X_test)[:5]

array([[0.4873288 , 0.5126712 ],

[0.47623584, 0.52376416],

[0.46529531, 0.53470469],

[0.47484469, 0.52515531],

[0.49020587, 0.50979413]])

K-Nearest Neighbors#

We will now perform KNN using the KNeighborsClassifier() function. This function works similarly

to the other model-fitting functions that we have

encountered thus far.

As is the

case for LDA and QDA, we fit the classifier

using the fit method. New

predictions are formed using the predict method

of the object returned by fit().

knn1 = KNeighborsClassifier(n_neighbors=1)

X_train, X_test = [np.asarray(X) for X in [X_train, X_test]]

knn1.fit(X_train, L_train)

knn1_pred = knn1.predict(X_test)

confusion_table(knn1_pred, L_test)

| Truth | Down | Up |

|---|---|---|

| Predicted | ||

| Down | 43 | 58 |

| Up | 68 | 83 |

The results using \(K=1\) are not very good, since only \(50%\) of the observations are correctly predicted. Of course, it may be that \(K=1\) results in an overly-flexible fit to the data.

(83+43)/252, np.mean(knn1_pred == L_test)

(0.5, np.float64(0.5))

We repeat the analysis below using \(K=3\).

knn3 = KNeighborsClassifier(n_neighbors=3)

knn3_pred = knn3.fit(X_train, L_train).predict(X_test)

np.mean(knn3_pred == L_test)

np.float64(0.5317460317460317)

The results have improved slightly. But increasing K further provides no further improvements. It appears that for these data, and this train/test split, QDA gives the best results of the methods that we have examined so far.

KNN does not perform well on the Smarket data, but it often does provide impressive results. As an example we will apply the KNN approach to the Caravan data set, which is part of the ISLP library. This data set includes 85

predictors that measure demographic characteristics for 5,822

individuals. The response variable is Purchase, which

indicates whether or not a given individual purchases a caravan

insurance policy. In this data set, only 6% of people purchased

caravan insurance.

Caravan = load_data('Caravan')

Purchase = Caravan.Purchase

Purchase.value_counts()

Purchase

No 5474

Yes 348

Name: count, dtype: int64

The method value_counts() takes a pd.Series or pd.DataFrame and returns

a pd.Series with the corresponding counts

for each unique element. In this case Purchase has only Yes and No values

and the method returns how many values of each there are.

348 / 5822

0.05977327378907592

Our features will include all columns except Purchase.

feature_df = Caravan.drop(columns=['Purchase'])

Because the KNN classifier predicts the class of a given test

observation by identifying the observations that are nearest to it,

the scale of the variables matters. Any variables that are on a large

scale will have a much larger effect on the distance between

the observations, and hence on the KNN classifier, than variables that

are on a small scale. For instance, imagine a data set that contains

two variables, salary and age (measured in dollars

and years, respectively). As far as KNN is concerned, a difference of

1,000 USD in salary is enormous compared to a difference of 50 years in

age. Consequently, salary will drive the KNN classification

results, and age will have almost no effect. This is contrary

to our intuition that a salary difference of 1,000 USD is quite small

compared to an age difference of 50 years. Furthermore, the

importance of scale to the KNN classifier leads to another issue: if

we measured salary in Japanese yen, or if we measured

age in minutes, then we’d get quite different classification

results from what we get if these two variables are measured in

dollars and years.

A good way to handle this problem is to standardize the data so that all variables are

given a mean of zero and a standard deviation of one. Then all

variables will be on a comparable scale. This is accomplished

using

the StandardScaler()

transformation.

scaler = StandardScaler(with_mean=True,

with_std=True,

copy=True)

The argument with_mean indicates whether or not

we should subtract the mean, while with_std indicates

whether or not we should scale the columns to have standard

deviation of 1 or not. Finally, the argument copy=True

indicates that we will always copy data, rather than

trying to do calculations in place where possible.

This transformation can be fit

and then applied to arbitrary data. In the first line

below, the parameters for the scaling are computed and

stored in scaler, while the second line actually

constructs the standardized set of features.

scaler.fit(feature_df)

X_std = scaler.transform(feature_df)

Now every column of feature_std below has a standard deviation of

one and a mean of zero.

feature_std = pd.DataFrame(

X_std,

columns=feature_df.columns);

feature_std.std()

MOSTYPE 1.000086

MAANTHUI 1.000086

MGEMOMV 1.000086

MGEMLEEF 1.000086

MOSHOOFD 1.000086

...

AZEILPL 1.000086

APLEZIER 1.000086

AFIETS 1.000086

AINBOED 1.000086

ABYSTAND 1.000086

Length: 85, dtype: float64

Notice that the standard deviations are not quite \(1\) here; this is again due to some procedures using the \(1/n\) convention for variances (in this case scaler()), while others use \(1/(n-1)\) (the std() method). See the footnote on page 183.

In this case it does not matter, as long as the variables are all on the same scale.

Using the function train_test_split() we now split the observations into a test set,

containing 1000 observations, and a training set containing the remaining

observations. The argument random_state=0 ensures that we get

the same split each time we rerun the code.

(X_train,

X_test,

y_train,

y_test) = train_test_split(np.asarray(feature_std),

Purchase,

test_size=1000,

random_state=0)

?train_test_split reveals that the non-keyword arguments can be lists, arrays, pandas dataframes etc that all have the same length (shape[0]) and hence are indexable. In this case they are the dataframe feature_std and the response variable Purchase.

{Note that we have converted feature_std to an ndarray to address a bug in sklearn.}

We fit a KNN model on the training data using \(K=1\),

and evaluate its performance on the test data.

knn1 = KNeighborsClassifier(n_neighbors=1)

knn1_pred = knn1.fit(X_train, y_train).predict(X_test)

np.mean(y_test != knn1_pred), np.mean(y_test != "No")

(np.float64(0.113), np.float64(0.067))

The KNN error rate on the 1,000 test observations is about \(11%\).

At first glance, this may appear to be fairly good. However, since

just over 6% of customers purchased insurance, we could get the error

rate down to almost 6% by always predicting No regardless of the

values of the predictors! This is known as the null rate.}

Suppose that there is some non-trivial cost to trying to sell insurance to a given individual. For instance, perhaps a salesperson must visit each potential customer. If the company tries to sell insurance to a random selection of customers, then the success rate will be only 6%, which may be far too low given the costs involved. Instead, the company would like to try to sell insurance only to customers who are likely to buy it. So the overall error rate is not of interest. Instead, the fraction of individuals that are correctly predicted to buy insurance is of interest.

confusion_table(knn1_pred, y_test)

| Truth | No | Yes |

|---|---|---|

| Predicted | ||

| No | 878 | 58 |

| Yes | 55 | 9 |

It turns out that KNN with \(K=1\) does far better than random guessing among the customers that are predicted to buy insurance. Among 62 such customers, 9, or 14.5%, actually do purchase insurance. This is double the rate that one would obtain from random guessing.

9/(53+9)

0.14516129032258066

Tuning Parameters#

The number of neighbors in KNN is referred to as a tuning parameter, also referred to as a hyperparameter.

We do not know a priori what value to use. It is therefore of interest

to see how the classifier performs on test data as we vary these

parameters. This can be achieved with a for loop, described in Section 2.3.8.

Here we use a for loop to look at the accuracy of our classifier in the group predicted to purchase

insurance as we vary the number of neighbors from 1 to 5:

for K in range(1,6):

knn = KNeighborsClassifier(n_neighbors=K)

knn_pred = knn.fit(X_train, y_train).predict(X_test)

C = confusion_table(knn_pred, y_test)

templ = ('K={0:d}: # predicted to rent: {1:>2},' +

' # who did rent {2:d}, accuracy {3:.1%}')

pred = C.loc['Yes'].sum()

did_rent = C.loc['Yes','Yes']

print(templ.format(

K,

pred,

did_rent,

did_rent / pred))

K=1: # predicted to rent: 64, # who did rent 9, accuracy 14.1%

K=2: # predicted to rent: 6, # who did rent 1, accuracy 16.7%

K=3: # predicted to rent: 20, # who did rent 3, accuracy 15.0%

K=4: # predicted to rent: 4, # who did rent 0, accuracy 0.0%

K=5: # predicted to rent: 7, # who did rent 1, accuracy 14.3%

We see some variability — the numbers for K=4 are very different from the rest.

Comparison to Logistic Regression#

As a comparison, we can also fit a logistic regression model to the

data. This can also be done

with sklearn, though by default it fits

something like the ridge regression version

of logistic regression, which we introduce in Chapter 6. This can

be modified by appropriately setting the argument C below. Its default

value is 1 but by setting it to a very large number, the algorithm converges to the same solution as the usual (unregularized)

logistic regression estimator discussed above.

Unlike the

statsmodels package, sklearn focuses less on

inference and more on classification. Hence,

the summary methods seen in statsmodels

and our simplified version seen with summarize are not

generally available for the classifiers in sklearn.

logit = LogisticRegression(C=1e10, solver='liblinear')

logit.fit(X_train, y_train)

logit_pred = logit.predict_proba(X_test)

logit_labels = np.where(logit_pred[:,1] > .5, 'Yes', 'No')

confusion_table(logit_labels, y_test)

| Truth | No | Yes |

|---|---|---|

| Predicted | ||

| No | 931 | 67 |

| Yes | 2 | 0 |

We used the argument solver='liblinear' above to

avoid a warning with the default solver which would indicate that

the algorithm does not converge.

If we use \(0.5\) as the predicted probability cut-off for the classifier, then we have a problem: only two of the test observations are predicted to purchase insurance. However, we are not required to use a cut-off of \(0.5\). If we instead predict a purchase any time the predicted probability of purchase exceeds \(0.25\), we get much better results: we predict that 29 people will purchase insurance, and we are correct for about 31% of these people. This is almost five times better than random guessing!

logit_labels = np.where(logit_pred[:,1]>0.25, 'Yes', 'No')

confusion_table(logit_labels, y_test)

| Truth | No | Yes |

|---|---|---|

| Predicted | ||

| No | 913 | 58 |

| Yes | 20 | 9 |

9/(20+9)

0.3103448275862069

Linear and Poisson Regression on the Bikeshare Data#

Here we fit linear and Poisson regression models to the Bikeshare data, as described in Section 4.6.

The response bikers measures the number of bike rentals per hour

in Washington, DC in the period 2010–2012.

Bike = load_data('Bikeshare')

Let’s have a peek at the dimensions and names of the variables in this dataframe.

Bike.shape, Bike.columns

((8645, 15),

Index(['season', 'mnth', 'day', 'hr', 'holiday', 'weekday', 'workingday',

'weathersit', 'temp', 'atemp', 'hum', 'windspeed', 'casual',

'registered', 'bikers'],

dtype='str'))

Linear Regression#

We begin by fitting a linear regression model to the data.

X = MS(['mnth',

'hr',

'workingday',

'temp',

'weathersit']).fit_transform(Bike)

Y = Bike['bikers']

M_lm = sm.OLS(Y, X).fit()

summarize(M_lm)

| coef | std err | t | P>|t| | |

|---|---|---|---|---|

| intercept | -68.6317 | 5.307 | -12.932 | 0.000 |

| mnth[Feb] | 6.8452 | 4.287 | 1.597 | 0.110 |

| mnth[March] | 16.5514 | 4.301 | 3.848 | 0.000 |

| mnth[April] | 41.4249 | 4.972 | 8.331 | 0.000 |

| mnth[May] | 72.5571 | 5.641 | 12.862 | 0.000 |

| mnth[June] | 67.8187 | 6.544 | 10.364 | 0.000 |

| mnth[July] | 45.3245 | 7.081 | 6.401 | 0.000 |

| mnth[Aug] | 53.2430 | 6.640 | 8.019 | 0.000 |

| mnth[Sept] | 66.6783 | 5.925 | 11.254 | 0.000 |

| mnth[Oct] | 75.8343 | 4.950 | 15.319 | 0.000 |

| mnth[Nov] | 60.3100 | 4.610 | 13.083 | 0.000 |

| mnth[Dec] | 46.4577 | 4.271 | 10.878 | 0.000 |

| hr[1] | -14.5793 | 5.699 | -2.558 | 0.011 |

| hr[2] | -21.5791 | 5.733 | -3.764 | 0.000 |

| hr[3] | -31.1408 | 5.778 | -5.389 | 0.000 |

| hr[4] | -36.9075 | 5.802 | -6.361 | 0.000 |

| hr[5] | -24.1355 | 5.737 | -4.207 | 0.000 |

| hr[6] | 20.5997 | 5.704 | 3.612 | 0.000 |

| hr[7] | 120.0931 | 5.693 | 21.095 | 0.000 |

| hr[8] | 223.6619 | 5.690 | 39.310 | 0.000 |

| hr[9] | 120.5819 | 5.693 | 21.182 | 0.000 |

| hr[10] | 83.8013 | 5.705 | 14.689 | 0.000 |

| hr[11] | 105.4234 | 5.722 | 18.424 | 0.000 |

| hr[12] | 137.2837 | 5.740 | 23.916 | 0.000 |

| hr[13] | 136.0359 | 5.760 | 23.617 | 0.000 |

| hr[14] | 126.6361 | 5.776 | 21.923 | 0.000 |

| hr[15] | 132.0865 | 5.780 | 22.852 | 0.000 |

| hr[16] | 178.5206 | 5.772 | 30.927 | 0.000 |

| hr[17] | 296.2670 | 5.749 | 51.537 | 0.000 |

| hr[18] | 269.4409 | 5.736 | 46.976 | 0.000 |

| hr[19] | 186.2558 | 5.714 | 32.596 | 0.000 |

| hr[20] | 125.5492 | 5.704 | 22.012 | 0.000 |

| hr[21] | 87.5537 | 5.693 | 15.378 | 0.000 |

| hr[22] | 59.1226 | 5.689 | 10.392 | 0.000 |

| hr[23] | 26.8376 | 5.688 | 4.719 | 0.000 |

| workingday | 1.2696 | 1.784 | 0.711 | 0.477 |

| temp | 157.2094 | 10.261 | 15.321 | 0.000 |

| weathersit[cloudy/misty] | -12.8903 | 1.964 | -6.562 | 0.000 |

| weathersit[heavy rain/snow] | -109.7446 | 76.667 | -1.431 | 0.152 |

| weathersit[light rain/snow] | -66.4944 | 2.965 | -22.425 | 0.000 |

There are 24 levels in hr and 40 rows in all.

In M_lm, the first levels hr[0] and mnth[Jan] are treated

as the baseline values, and so no coefficient estimates are provided

for them: implicitly, their coefficient estimates are zero, and all

other levels are measured relative to these baselines. For example,

the Feb coefficient of \(6.845\) signifies that, holding all other

variables constant, there are on average about 7 more riders in

February than in January. Similarly there are about 16.5 more riders

in March than in January.

The results seen in Section 4.6.1

used a slightly different coding of the variables hr and mnth, as follows:

hr_encode = contrast('hr', 'sum')

mnth_encode = contrast('mnth', 'sum')

Refitting again:

X2 = MS([mnth_encode,

hr_encode,

'workingday',

'temp',

'weathersit']).fit_transform(Bike)

M2_lm = sm.OLS(Y, X2).fit()

S2 = summarize(M2_lm)

S2

| coef | std err | t | P>|t| | |

|---|---|---|---|---|

| intercept | 73.5974 | 5.132 | 14.340 | 0.000 |

| mnth[Jan] | -46.0871 | 4.085 | -11.281 | 0.000 |

| mnth[Feb] | -39.2419 | 3.539 | -11.088 | 0.000 |

| mnth[March] | -29.5357 | 3.155 | -9.361 | 0.000 |

| mnth[April] | -4.6622 | 2.741 | -1.701 | 0.089 |

| mnth[May] | 26.4700 | 2.851 | 9.285 | 0.000 |

| mnth[June] | 21.7317 | 3.465 | 6.272 | 0.000 |

| mnth[July] | -0.7626 | 3.908 | -0.195 | 0.845 |

| mnth[Aug] | 7.1560 | 3.535 | 2.024 | 0.043 |

| mnth[Sept] | 20.5912 | 3.046 | 6.761 | 0.000 |

| mnth[Oct] | 29.7472 | 2.700 | 11.019 | 0.000 |

| mnth[Nov] | 14.2229 | 2.860 | 4.972 | 0.000 |

| hr[0] | -96.1420 | 3.955 | -24.307 | 0.000 |

| hr[1] | -110.7213 | 3.966 | -27.916 | 0.000 |

| hr[2] | -117.7212 | 4.016 | -29.310 | 0.000 |

| hr[3] | -127.2828 | 4.081 | -31.191 | 0.000 |

| hr[4] | -133.0495 | 4.117 | -32.319 | 0.000 |

| hr[5] | -120.2775 | 4.037 | -29.794 | 0.000 |

| hr[6] | -75.5424 | 3.992 | -18.925 | 0.000 |

| hr[7] | 23.9511 | 3.969 | 6.035 | 0.000 |

| hr[8] | 127.5199 | 3.950 | 32.284 | 0.000 |

| hr[9] | 24.4399 | 3.936 | 6.209 | 0.000 |

| hr[10] | -12.3407 | 3.936 | -3.135 | 0.002 |

| hr[11] | 9.2814 | 3.945 | 2.353 | 0.019 |

| hr[12] | 41.1417 | 3.957 | 10.397 | 0.000 |

| hr[13] | 39.8939 | 3.975 | 10.036 | 0.000 |

| hr[14] | 30.4940 | 3.991 | 7.641 | 0.000 |

| hr[15] | 35.9445 | 3.995 | 8.998 | 0.000 |

| hr[16] | 82.3786 | 3.988 | 20.655 | 0.000 |

| hr[17] | 200.1249 | 3.964 | 50.488 | 0.000 |

| hr[18] | 173.2989 | 3.956 | 43.806 | 0.000 |

| hr[19] | 90.1138 | 3.940 | 22.872 | 0.000 |

| hr[20] | 29.4071 | 3.936 | 7.471 | 0.000 |

| hr[21] | -8.5883 | 3.933 | -2.184 | 0.029 |

| hr[22] | -37.0194 | 3.934 | -9.409 | 0.000 |

| workingday | 1.2696 | 1.784 | 0.711 | 0.477 |

| temp | 157.2094 | 10.261 | 15.321 | 0.000 |

| weathersit[cloudy/misty] | -12.8903 | 1.964 | -6.562 | 0.000 |

| weathersit[heavy rain/snow] | -109.7446 | 76.667 | -1.431 | 0.152 |

| weathersit[light rain/snow] | -66.4944 | 2.965 | -22.425 | 0.000 |

What is the difference between the two codings? In M2_lm, a

coefficient estimate is reported for all but level 23 of hr

and level Dec of mnth. Importantly, in M2_lm, the (unreported) coefficient estimate

for the last level of mnth is not zero: instead, it equals the

negative of the sum of the coefficient estimates for all of the

other levels. Similarly, in M2_lm, the coefficient estimate

for the last level of hr is the negative of the sum of the

coefficient estimates for all of the other levels. This means that the

coefficients of hr and mnth in M2_lm will always sum

to zero, and can be interpreted as the difference from the mean

level. For example, the coefficient for January of \(-46.087\) indicates

that, holding all other variables constant, there are typically 46

fewer riders in January relative to the yearly average.

It is important to realize that the choice of coding really does not matter, provided that we interpret the model output correctly in light of the coding used. For example, we see that the predictions from the linear model are the same regardless of coding:

np.sum((M_lm.fittedvalues - M2_lm.fittedvalues)**2)

np.float64(1.3065272798976998e-19)

The sum of squared differences is zero. We can also see this using the

np.allclose() function:

np.allclose(M_lm.fittedvalues, M2_lm.fittedvalues)

True

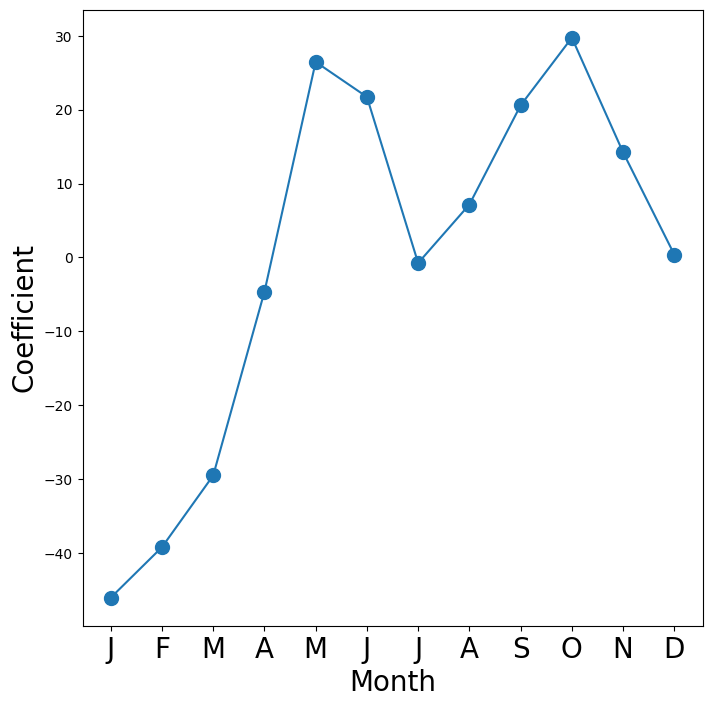

To reproduce the left-hand side of Figure 4.13

we must first obtain the coefficient estimates associated with

mnth. The coefficients for January through November can be obtained

directly from the M2_lm object. The coefficient for December

must be explicitly computed as the negative sum of all the other

months. We first extract all the coefficients for month from

the coefficients of M2_lm.

coef_month = S2[S2.index.str.contains('mnth')]['coef']

coef_month

mnth[Jan] -46.0871

mnth[Feb] -39.2419

mnth[March] -29.5357

mnth[April] -4.6622

mnth[May] 26.4700

mnth[June] 21.7317

mnth[July] -0.7626

mnth[Aug] 7.1560

mnth[Sept] 20.5912

mnth[Oct] 29.7472

mnth[Nov] 14.2229

Name: coef, dtype: float64

Next, we append Dec as the negative of the sum of all other months.

months = Bike['mnth'].dtype.categories

coef_month = pd.concat([

coef_month,

pd.Series([-coef_month.sum()],

index=['mnth[Dec]'

])

])

coef_month

mnth[Jan] -46.0871

mnth[Feb] -39.2419

mnth[March] -29.5357

mnth[April] -4.6622

mnth[May] 26.4700

mnth[June] 21.7317

mnth[July] -0.7626

mnth[Aug] 7.1560

mnth[Sept] 20.5912

mnth[Oct] 29.7472

mnth[Nov] 14.2229

mnth[Dec] 0.3705

dtype: float64

Finally, to make the plot neater, we’ll just use the first letter of each month, which is the \(6\)th entry of each of the labels in the index.

fig_month, ax_month = subplots(figsize=(8,8))

x_month = np.arange(coef_month.shape[0])

ax_month.plot(x_month, coef_month, marker='o', ms=10)

ax_month.set_xticks(x_month)

ax_month.set_xticklabels([l[5] for l in coef_month.index], fontsize=20)

ax_month.set_xlabel('Month', fontsize=20)

ax_month.set_ylabel('Coefficient', fontsize=20);

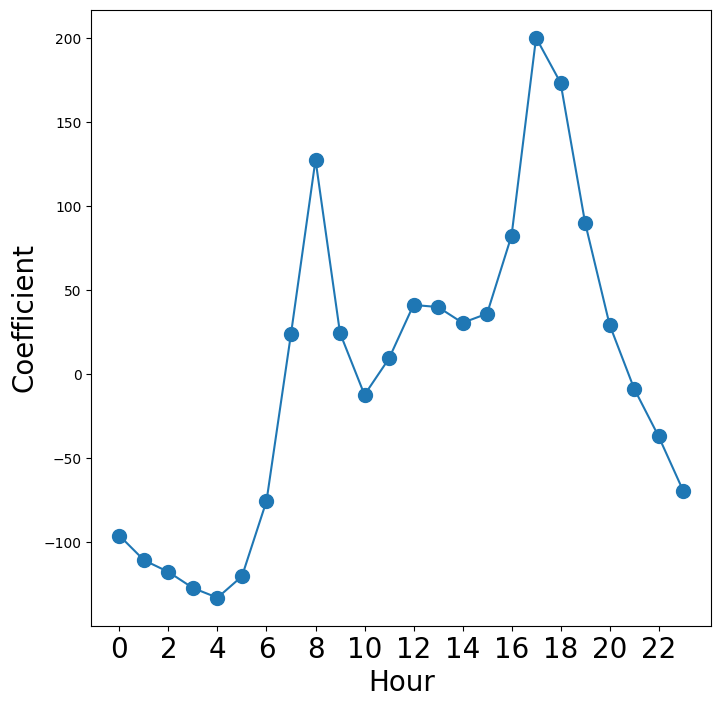

Reproducing the right-hand plot in Figure 4.13 follows a similar process.

coef_hr = S2[S2.index.str.contains('hr')]['coef']

coef_hr = coef_hr.reindex(['hr[{0}]'.format(h) for h in range(23)])

coef_hr = pd.concat([coef_hr,

pd.Series([-coef_hr.sum()], index=['hr[23]'])

])

We now make the hour plot.

fig_hr, ax_hr = subplots(figsize=(8,8))

x_hr = np.arange(coef_hr.shape[0])

ax_hr.plot(x_hr, coef_hr, marker='o', ms=10)

ax_hr.set_xticks(x_hr[::2])

ax_hr.set_xticklabels(range(24)[::2], fontsize=20)

ax_hr.set_xlabel('Hour', fontsize=20)

ax_hr.set_ylabel('Coefficient', fontsize=20);

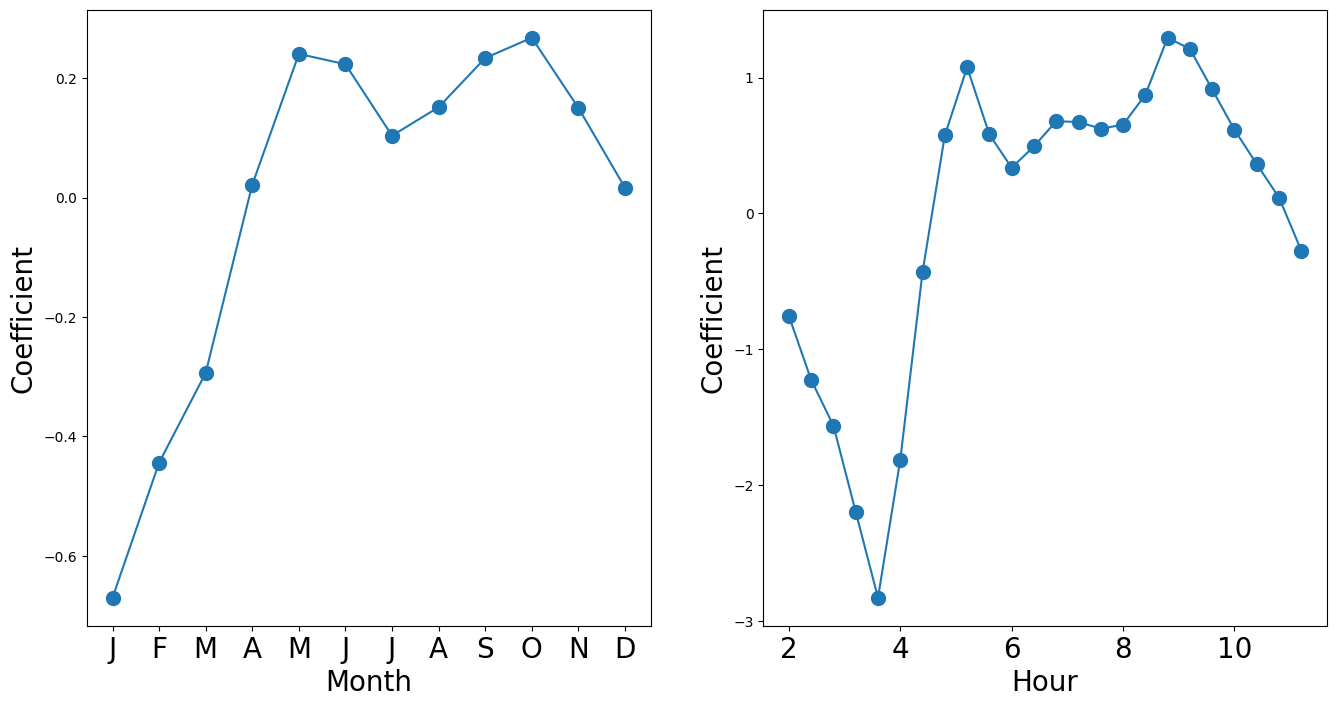

Poisson Regression#

Now we fit instead a Poisson regression model to the

Bikeshare data. Very little changes, except that we now use the

function sm.GLM() with the Poisson family specified:

M_pois = sm.GLM(Y, X2, family=sm.families.Poisson()).fit()

We can plot the coefficients associated with mnth and hr, in order to reproduce Figure 4.15. We first complete these coefficients as before.

S_pois = summarize(M_pois)

coef_month = S_pois[S_pois.index.str.contains('mnth')]['coef']

coef_month = pd.concat([coef_month,

pd.Series([-coef_month.sum()],

index=['mnth[Dec]'])])

coef_hr = S_pois[S_pois.index.str.contains('hr')]['coef']

coef_hr = pd.concat([coef_hr,

pd.Series([-coef_hr.sum()],

index=['hr[23]'])])

The plotting is as before.

fig_pois, (ax_month, ax_hr) = subplots(1, 2, figsize=(16,8))

ax_month.plot(x_month, coef_month, marker='o', ms=10)

ax_month.set_xticks(x_month)

ax_month.set_xticklabels([l[5] for l in coef_month.index], fontsize=20)

ax_month.set_xlabel('Month', fontsize=20)

ax_month.set_ylabel('Coefficient', fontsize=20)

ax_hr.plot(x_hr, coef_hr, marker='o', ms=10)

ax_hr.set_xticklabels(range(24)[::2], fontsize=20)

ax_hr.set_xlabel('Hour', fontsize=20)

ax_hr.set_ylabel('Coefficient', fontsize=20);

/var/folders/16/8y65_zv174qgdp4ktlmpv12h0000gq/T/ipykernel_26027/3779905754.py:8: UserWarning: set_ticklabels() should only be used with a fixed number of ticks, i.e. after set_ticks() or using a FixedLocator.

ax_hr.set_xticklabels(range(24)[::2], fontsize=20)

We compare the fitted values of the two models.

The fitted values are stored in the fittedvalues attribute

returned by the fit() method for both the linear regression and the Poisson

fits. The linear predictors are stored as the attribute lin_pred.

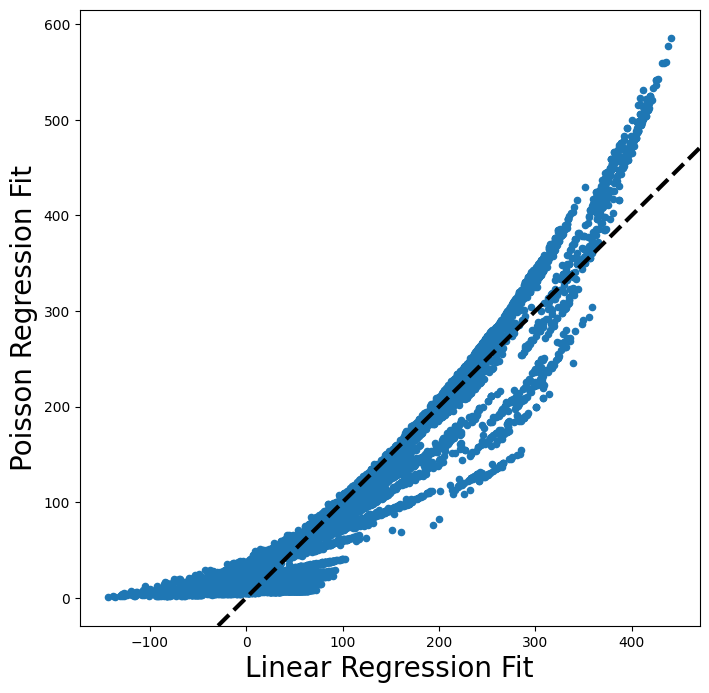

fig, ax = subplots(figsize=(8, 8))

ax.scatter(M2_lm.fittedvalues,

M_pois.fittedvalues,

s=20)

ax.set_xlabel('Linear Regression Fit', fontsize=20)

ax.set_ylabel('Poisson Regression Fit', fontsize=20)

ax.axline([0,0], c='black', linewidth=3,

linestyle='--', slope=1);

The predictions from the Poisson regression model are correlated with those from the linear model; however, the former are non-negative. As a result the Poisson regression predictions tend to be larger than those from the linear model for either very low or very high levels of ridership.

In this section, we fit Poisson regression models using the sm.GLM() function with the argument

family=sm.families.Poisson(). Earlier in this lab we used the sm.GLM() function

with family=sm.families.Binomial() to perform logistic regression. Other

choices for the family argument can be used to fit other types

of GLMs. For instance, family=sm.families.Gamma() fits a Gamma regression

model.